Wakala Meaning:

Wakala refers to a contract where a principal (or muwakkil) authorizes or appoints an agent (or wakeel) to do a well-defined legal action on his or her behalf. Wakala meaning in English is “Contract of an Agency”. The wakalah in Islamic banking is about the provision of service, and main features of wakalah are service, representation and power to affect the legal position of the principal.

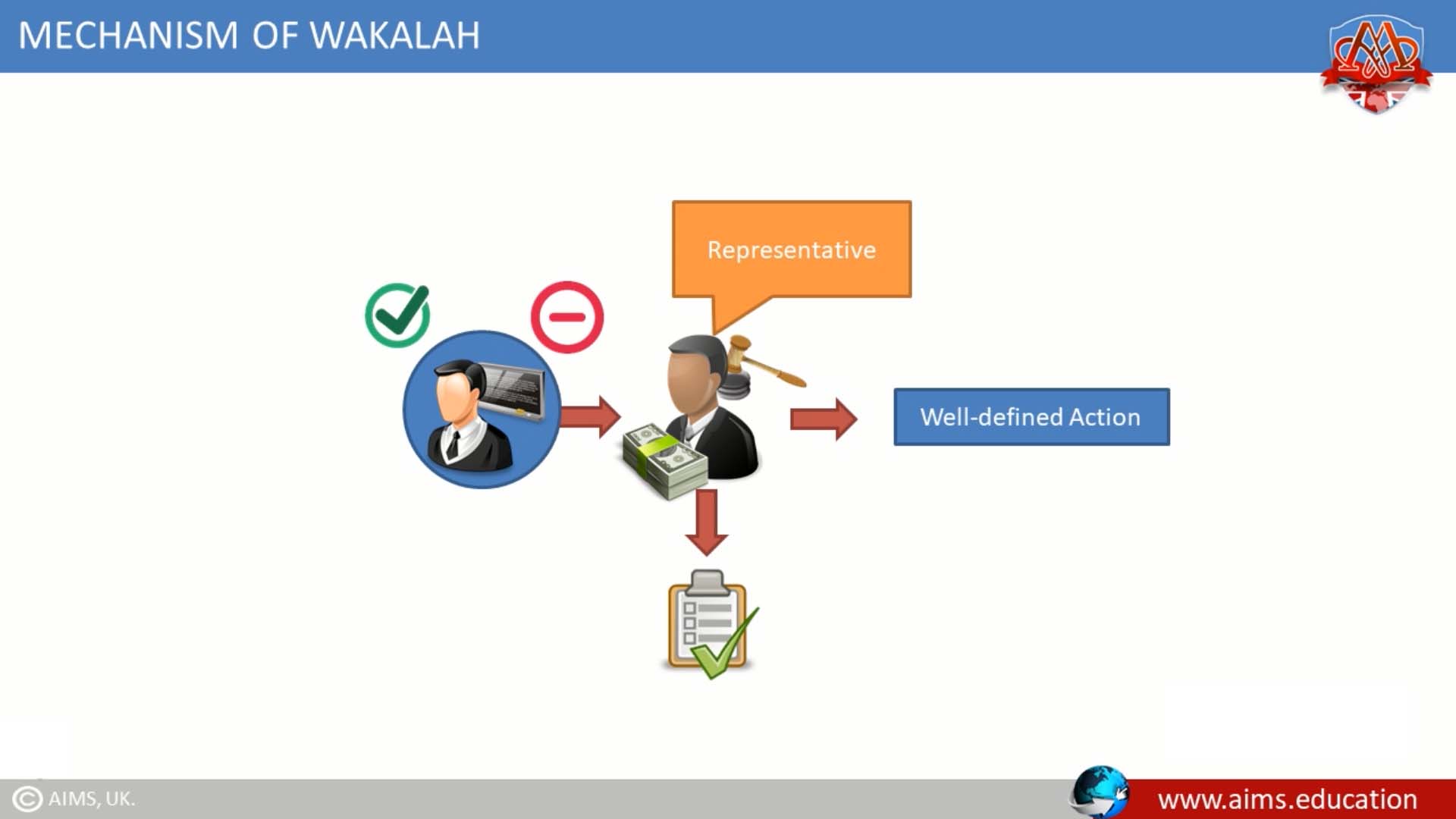

Wakalah in Islamic Banking:

Wakala in Islamic banking is used, where a representative is appointed to undertake transactions on another person’s behalf. The agency law or Wakala law is to facilitate economic exchanges, where they are hindered by distance, size, and numbers, or where principal is unable, or unwilling to act personally.

What is Wakalah Contract?

- Principal appoints an agent, to carry out a certain well-defined action, as a representative.

- Agent performs the task, according to the instructions.

- Agent is entitled to receive a predetermined fee, irrespective of whether the accomplished task satisfied the principal or not.

Conditions of Wakala in Islamic Banking:

- Agent should also be a competent person.

- Principal should have the power, and competence to deal. For example: an insane or a minor cannot appoint agents.

- Act should be known and must be lawful.

Types of Wakalah:

Particular Wakalah or Special Agency:

This agreement is made for a certain known transaction. For Example: Agent is bound to sell or buy a particular house or car.

General Wakalah:

It is a general delegation of power. For example: Principal asks an agent to buy a 4 bedroom house.

Restricted Agency:

Where agent acts within certain conditions; For Example: Buy the house on a certain price, and on in given time.

Absolute Agency:

Where no condition is put for the transaction; For Example: No specific price or time is given to agent.

Examples of Wakala:

For example, lawyers are employed to represent their clients, or brokers are authorized to sell or purchase commodities. Similarly, in organizations such as companies, managers and directors are needed to act on behalf of the companies.

In some cases, specialized middlemen are needed to make contracts on behalf of their principals or to dispose of their principals’ property. Commerce could come to a standstill if businessmen and merchants could not employ the services of agents and were expected to do everything themselves.

An agent may obtain a certain wage for his services. If payment is not mentioned, in this case reference is made to the practice of the people. For example, a lawyer or a broker is entitled to their wages based on the practice common among the people. Wakalah is a non-binding contract.

Wakala Deposit:

Wakala deposit is generally referred as a Shariah Compliant contract in which customer authorizes an Islamic bank to invest his/her funds in Shariah approved activities to earn profits.

Laws Concerning Wakalah in Islamic Banking & Finance:

Wakala in Islamic banking refers to the concept of a businessman entrusting another to act in his stead or as his representative. It has been a long-standing custom to appoint an agent to facilitate trade operations. Wakala is the most important element in Islamic partnerships and, in modern law, too, the relationship between partners is known as a principal-agent relationship.

The main laws concerning an agency are as follows:

- The essence of the appointment of an agent is the proposal and acceptance of the position or giving a person permission to act for one.

- The sending of a messenger is not of the same category as the appointment of an agent.

- A person who appoints an agent must be legally competent to do the work for which the agent is appointed. All insane person or an Infant cannot appoint all agent.

- A person who appoints an agent must have attained understanding and sound judgment but it is not necessary for him to be of age.

- A person may appoint all agent to conduct any business transaction that he would be able to do himself.

- When making contracts concerning gifts, loans for gratuitous use or deposits. Entering into partnerships or compromising on a matter denied by the other side, an agent should refer them to his principal.

- An agent appointed to buy and sell or to pay and receive a debt is considered to be a custodian of his principal’s property and in the position of a trustee (amin). If the property is destroyed without its being his fault or due to his negligence, no compensation can be claimed.

- An agent is entitled to receive remuneration only when so contracted.

An agent appointed to sell goods cannot buy then for himself without the principal’s consent. - In the absence of any instructions to the contrary, an agent appointed to sell goods can sell them for cash or on credit and can take a pledge or surety for the price of the goods sold on credit. But if the pledge is destroyed or the surety becomes bankrupt, the agent cannot be held responsible.

- The principal can dismiss his agent providing that this does not contravene the rights of others.

- An agent is considered discharged on the death of his principal provided that this does not contravene the rights of others.

- The agency becomes void on the principal becoming a lunatic. The wakalah and its contract is discussed in more details in the Islamic finance degree offered by AIMS’ institute of Islamic banking and finance.