What is Al Murabahah?

Murabahah is a contract wherein the Islamic Bank, upon request by the customer, purchases the asset from a third party supplier/vendor and resells it to the customer either against immediate payment or on a deferred payment basis. Basically Al Murabahah or Murabaha contract is the sale of goods at cost plus an agreed profit, and is also referred as commodity murabahah.

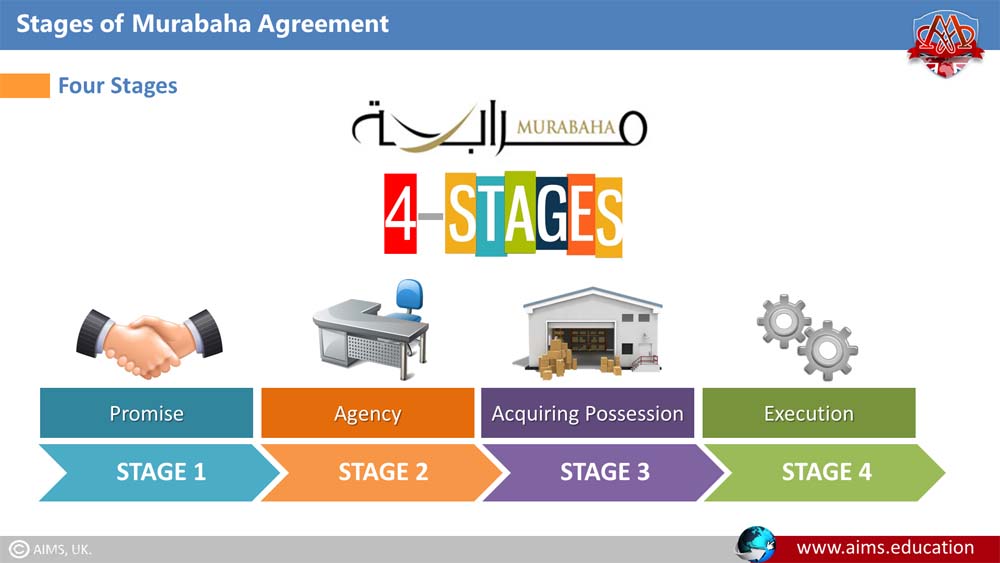

Stages of Murabaha Contract:

1. Promise Stage,

2. Agency Stage,

3. Acquiring Possession, and,

4. Execution.

Promise Stage:

Credit Approval:

The transaction parties must be genuine. The nature of business must be in scope of the Murabahah, and it should be Halal as well. Deferred payment not permissible in case of Gold, Silver and Currencies; however, after these consideration limit may be approved. After Credit approval, the Bank will sign Murabaha Agreement, and Sharia status of this agreement will be apromise MOU.

Purchase Requisition:

The Client orders the institution to buy certain goods for him and sell him the same after acquiring. The prerequisite is that the goods are not already owned by the client. At this stage of murabaha contract, the customer promises the institution to buy the goods which were acquired by the institute on his request.

Acquiring Possession:

Once the customer purchases the goods the risk of the goods transfers to the Bank. Bank can now sell these goods to the customer. Please note that the customer play two different roles in this transaction. One that of Bank’s agent and other of purchaser, and these roles should be clearly segregated to make the transaction Halal.

Acquisition of Title & Possession of the Asset:

Institution must take constructive or actual possession of the product being sold. And, goods must exist at the time of execution of Al Murabahah. The murabaha contract cannot be executed if the above two conditions are not fulfilled.

Basic Rules of Murabaha Agreement:

Conditions of Subject Matter:

Item must exists and must be in the ownership of the seller. Subject Matter of commodity murabahah must be in the physical or constructive possession of the seller (transfer of risk and reward and permission of use/Tasarruf). The subject of sale must be a property, of a value. Subject of Murabaha contract should not be a thing which is not used except for a Haram Purpose. The subject matter must be specifically known and identified to the buyer. The delivery of subject matter must be certain and should not depend on chance. The subject matter (such as murabaha mortgage or commodity murabahah) must be tangible goods and commodities. The exact cost of subject matter can be ascertained, and the subject matter is purchased by a third party.

Conditional Sale:

There are four types of conditions:

- Condition which is the requirement of sale (Valid).

- Reasonable condition for the safety of Subject mater (Valid).

- Unreasonable condition but in accordance with normal market practice (Valid).

- Condition which is Against the requirement of sale, Not in accordance with the market practice Beneficial for the seller or purchaser (void).

Price of Murabahah:

The price must be certain. (lump sum/by percentage). The price may be deferred or on spot, and if the price is deferred, the installments and due date must be determined. When the price is fixed it cannot be decreased incase of earlier payment, whereas, when the price is fixed it cannot be increased incase of default. Fluctuation price is not permissible. However, use of benchmark at the time of Master Financing Agreement is permissible.

Expenses of Al Murabahah:

The expenses incurred by the seller directly in acquiring the commodity like freight and custom duty can be included in the cost price.

Commodity Murabahah as a Mode of Financing:

It is a package of the following different contracts:

- Master financing agreement between bank and customer.

- Undertaking from client.

- Agency agreement between bank and customer.

- Purchase of goods from supplier.

- Agreement between bank and client.

The sequence between 3, 4 & 5 is extremely important.

Al Murabahah, its mechanism, accounting standards, shariah standards and its designing is discussed in more details during the Islamic banking course, mba Islamic finance and phd Islamic finance programs. Our next lecture is on Ijarah, which is an alternate of lease in Islamic banking and finance.