Modes of Islamic Banking and Finance:

Islamic financing is a transformation of Lending into Asset Based Financing, within the ambit of Shariah compliant business contracts, called Islamic Financial Instruments. The Islamic banking institutions first take ownership of the goods, which are being sold or rented. According to a well-known principle of Islamic jurisprudence, “One cannot earn profit from his capital or asset, unless he has have taken risk, or liability of ownership of that capital or asset”. Contrary to that, conventional banks earn interest by lending money. There are three main categories of modes of Islamic banking or Islamic banking instruments.

Types of Islamic Financial Instruments:

The three categories of Islamic financial instruments are:

- Debt Based or Trade Based products; such as Murabahah, Musawamah, Salam and Istisna.

- Equity Based products; such as, Musharakah and Mudarabah.

- Semi debt based; that is Ijarah.

In equity based products, the profit is shared on actual earning basis. Due to this reason, they are more risky than the other two categories, and so they are most preferred in Islamic Shariah.

Islamic Financial Products VS Conventional Products:

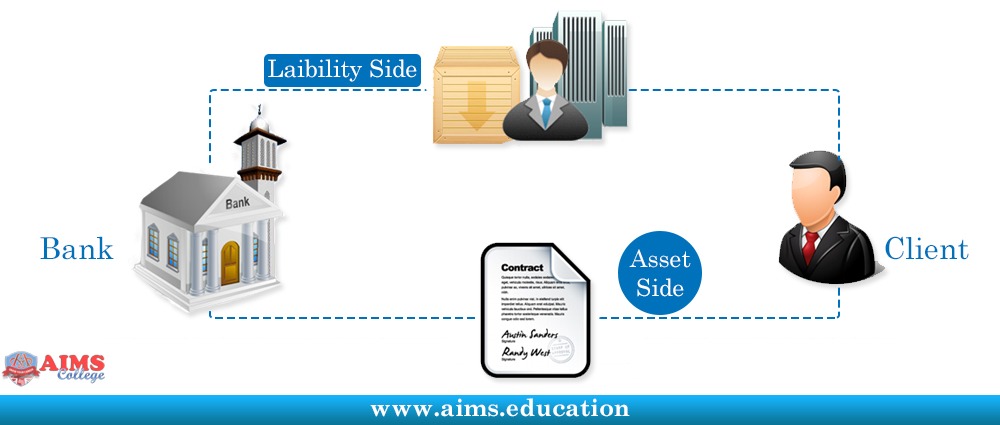

In case of conventional banking:

- For Asset side products, bank is the lender, and client is the borrower.

- For Liability side products, bank is the borrower, and client is the lender.

However, the case is different in Islamic banking and financial system, and the asset and liability sides of Islamic financial instruments are listed below:

| Liability Side Products | Asset Side Products |

| Musawamah Murabahah Salam Istisna Mudarabah Ijarah | Mudarabah Musharakah |

Shariah Contracts for Islamic Financial Instruments:

Given below is an overview of some major modes of financing in Islamic banking:

MUDARABAH CONTRACT:

An Islamic financial instrument, in which one party participates with money and the another with efforts. The profit shall be divided in strict proportion, and no party shall be entitled to a predetermined amount of return. Financial losses shall be borne solely by the investor.

MURABAHAH CONTRACT:

Murabahah refers to sale of goods and margin of profit is included in the sale price of goods. Subject of sale must exist, owned by seller and in his physical or constructive possession. So, the seller assumes the risks of ownership. Murabahah requires an offer and acceptance, which must include: Certainty of Price, Place of Delivery; and Date when Price will be paid.

IJARAH CONTRACT:

It generally means lease or rent, and it is a very popular Islamic mode of finance. Ijarah is selling of the benefit of use or service, for a fixed price or wage. The bank makes available an asset or equipment, such as plant, office automation, or motor vehicle, for a fixed period and rent. The corpus of leased commodity remains in the ownership of the lessor, and only its usufruct is transferred to the lessee.

MUSHARAKAH CONTRACT:

Musharakah is a business contract established by partners, who agree to share business profits and losses. Profits are distributed in the proportion mutually agreed in the contract. If one or more partners choose to become non-working partners, the ratio of their profit cannot exceed their ratio in the capital investment.

SALAM CONTRACT:

Salam is an Islamic mode of financing, where the seller undertakes to supply specific goods at future date, in consideration of a price fully paid in advance, at the time the contract. If full amount is not paid, it will be tantamount to a sale of debt against debt, which is Har-aam.

ISTISNA CONTRACT:

It is one of the Islamic banking instruments where buyer places an order to manufacture, assemble or construct something at an agreed price, and to be delivered at a future date. Commodity must be known and specified, such as its kind, type, quality and quantity. Price must also be fixed in absolute and unambiguous terms, and it can be paid in lump sum or in installments, as mutually agreed.

Applications of Islamic Financial Instruments:

- Murabahah is used for Trade Transactions, Working Capital Finance, and Fixed Assets Financing.

- Musharakah is used for Working Capital or Running Financing, Term Finance for Joint venture, and Equity Participation.

- Diminishing Musharakah is used for Asset Financing, such as Car, House and Shop.

- Ijarah or leasing is used for the financing of Auto, Building, Machinery, and Equipment.

- Istisna is used to Finance: Manufacturing Goods, Construction of Building, Exports, and Pay the overhead expenses like, salaries and utility bills.

- Salam is used for Agriculture or Commodity financing.