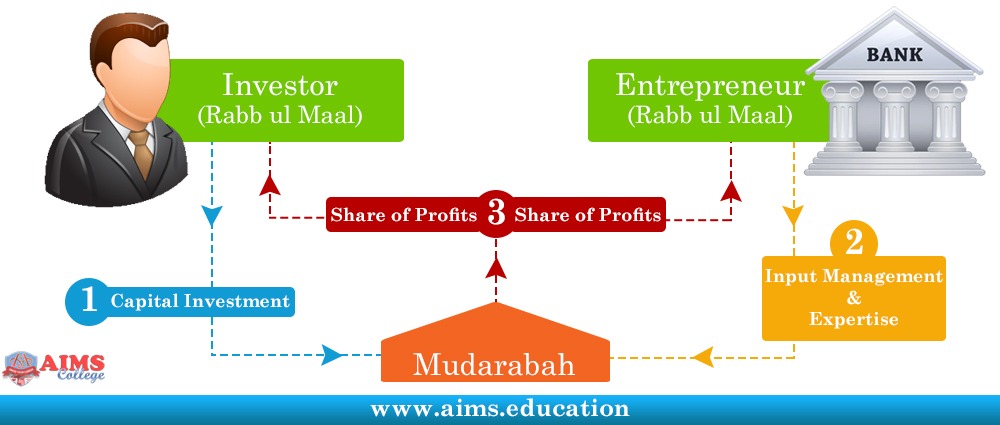

Mudarabah Definition:

Mudarabah contract is a business partnership contract. Let us first understand, what is mudarabah definition: “A partnership, where one partner invests in a business venture, while the other manages the business”. In mudaraba, the person investing is called Rabb-ul-maal, the person who manages the business is called Mudarib, and the investment is called “Raas-ul-Maal”. Here is a Mudarabah example: Two partners plan to open a car show room. The investing partner or Rabb-ul-maal will be responsible to make the investment for buying the cars, paying the rent, and make other office expenses. Whereas, Mudarib as a working partner, is responsible to provide skill, expertise and business management. Mudarabah in Islamic banking is widely used to structure bank deposit accounts, and it is also used in combination with other Islamic financial contracts.

Types of Mudarabah:

It is divided into two types: Restricted and Un-Restricted.

Restricted Mudarabah:

It is a contract, in which investor restricts the actions of working partner to particular location, or to a particular type of business.

Unrestricted Mudarabah:

In mudarabah contract, investor permits the working partner to administer the fund, without any restrictions.

Mudarabah Contract:

- Investor and Working Partner decide to enter a business venture.

- Investor provides capital to run the business, and Working Partner is responsible to run and manage the business through his expertise.

- Subsequently, if the venture is successful and generates profit, this profit is distributed among both partners, on a pre-determined ratio.

Mudarabah Example – Islamic Bank Accounts:

Islamic Current Account:

In Islamic Bank, current accounts are opened on the basis of “Loan” to bank, so the principal is guaranteed, and no facility can be given to the account holders.

Islamic Saving Accounts:

- They are term-deposit in a combination of Shirkah and Mudarabah.

- Constructive liquidation is done every month, or half yearly.

- Physical liquidation is usually not possible in banking system.

- While calculating the profit ratio, “Administrative Expenses” are deducted from depositors, and branch or operational expenses are deducted from total portfolio.

Islamic Project Financing:

If the Financier wants to finance the whole project, it is Mudarabah. However, if the investment comes from both sides, it is Musharkah.

Islamic Working Capital:

Working capital finance could be provided only through Musharkah financing. Amount invested by the Financier, will be treated as its’ share of investment. Financier’s share in profit should not exceed the percentage of its investment.

Mudaraba with Other Islamic Modes:

- Under the principle of Mudarabah, customer is an Investor and bank is the manager of funds deposited by the customer.

- Bank allocates those funds to a deposit or investment pool.

- Pool funds are used to provide financing to customers, under Islamic modes, such as: Murabahah, Ijarah, Istisna, Musharakah, Diminishing Musharakah, etc

- Profits earned through these modes are distributed among the bank and depositors.

Combining Musharakah and Mudaraba:

Working Partner may also invest money in the business, and in this case, Mu-shaar-kah and Mudaraba are combined.

Case Study:

“Ali” and “Bilal” starts a Mudarabah business, and it is agreed that “Bilal” will invest $100,000, and “Ali” will share the profit as a working partner, on an agreed ratio. Suppose that after some time, more investment is needed, and “Ali” adds $50,000 with the permission of “Bilal”. So, in that case “Ali” will take profit:

- As an “Investor” against his investment of $50,000; and;

- As a “Working Partner” for managing the whole business worth $150,000.

Two-Tier Mudarabah in Islamic Banking:

Almost all Islamic Banks are using this Mudaraba based liability structure, where:

- Bank first sign an agreement with the depositors, as a Managing Partner of their funds, and;

- Then the banks sign an agreement with the Entrepreneur, as an Investor.

This model is a hybrid of both Musharakah and Mudaraba. Islamic bank also commingles Islamic Banking Fund, especially when there is single pool for PLS based deposit products. This topic is discussed in more details, in the Islamic finance certificate, which is a part of our diploma in Islamic banking and finance. In the next lecture, you will understand the concept and examples of takaful Insurance.