What is Diminishing Musharakah?

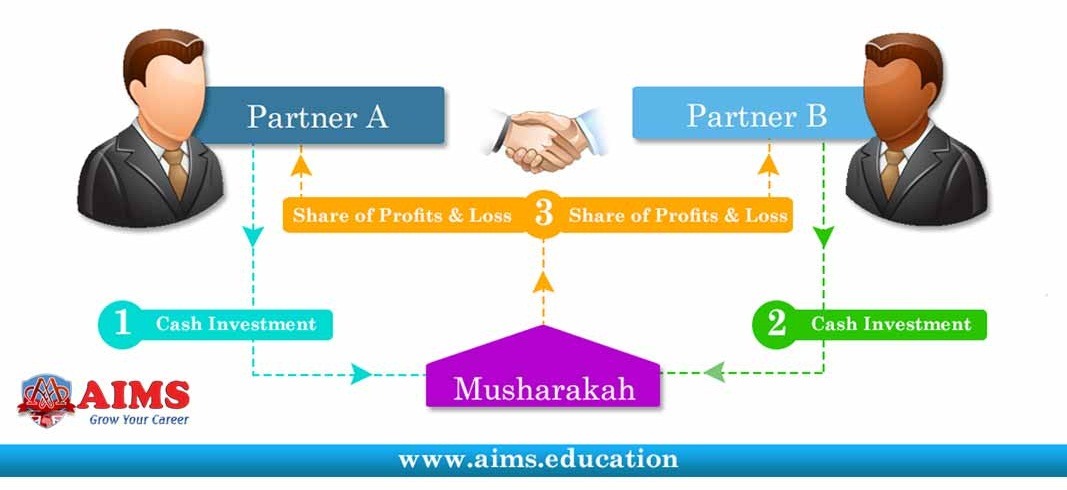

Diminishing Musharakah is a type of Shirkah, where one partner purchases the shares of the other partner, gradually. According to the concept of Diminishing Musharaka, an investor jointly own fixed asset with another person. Diminishing musharakah example asset could be a house, car, plan, or machinery. Shares of the investor are then divided into units, and it is pre-agreed that the person will purchase all those units over a period of time, and will become a sole owner of that asset. It is also called “Shirkah Al Mutanaqisah”. There are two types of diminishing musharakah: Shirkat-Ul-Aaqd and Shirkat-Ul-Milk.

Diminishing Musharakah Definition:

The proposed arrangement is composed of the following transactions:

- To create joint ownership in the property (Shirkat-ul-Milk).

- Giving the share of the financier to the client on rent.

- Promise from the client to purchase the units of share of the financier.

- Actual purchase of the units at different stages.

Diminishing Musharakah Example and Mechanism:

It based on the above concept has taken different shapes in different transactions. It is widely used for house financing. Here is a diminishing musharakah example:

- The client wants to purchase a house for which he does not have adequate funds. It approaches the financier who agrees to participate with him in purchasing the required house 20% of the price is paid by the client and 80% of the price by the financier. Thus, the financier owns 80% of the house while the client owns 20%. After purchasing the property jointly, the client uses the house for his residential requirement and pays rent to the financier for using his share in the property. At the same time, the share of financier is further divided in eight equal units, each unit representing 10% ownership of the house. The client promises to the financier that he will purchase one unit after three months. Accordingly months, he purchases one unit of the share of the financier by paying 1/10th of the price of the house. It reduces the share of the financier from 80% to 70%. Finance, the rent payable to the financier is also reduced to that extent. At the end of the second term, he purchases another unit increasing his share in the property to 40% and reducing the share of the financier to 60% and consequently reducing the rent to that proportion. This process goes on in the same fashion until after the end of two years, the client purchases the whole share of the financier reducing the share of the financier to ‘zero’ and increasing his own share to 100%

- This arrangement allows the financier to claim rent according to his proportion of ownership in the property and at the same time allows him periodical return of a part of his principal through purchases of the units of his share.

- ‘A’ wants to purchase a taxi to use it for offering transport services to passengers and to earn income through fares recovered from them, but he is short of funds. ‘B’ agrees to participate in the purchase of the taxi, therefore, both of them purchase a taxi jointly. 80% of the price is paid by ‘B’ and 20% is paid by A. After the taxi is purchased, it is employed to provide transport to the passengers whereby the net income of $1000/- is earned on daily basis. Since ‘B’ has 80% share in the taxi, it is agreed that 80% of the fare will be given to him and the rest of 20% will be retained by ‘A’ who has a 20% share in the taxi. It means that $800/- is earned by ‘B’ and $200/- by ‘A’ on daily basis. At the same time the share of ‘B’ is further divided into eight units. After three months ‘A’ purchases one unit from the share of ‘B’. Consequently the share of ‘B’ is reduced to 70% and share of ‘A’ is increased, after the first term of three months increased to 30% meaning thereby that as from that date ‘A’ will be entitled to $300/- from the daily income of the taxi and ‘B’ will earn $700/-. This process will go on until after the expiry of two years, the whole taxi will be owned by ‘A’ and ‘B’ will take back his original investment along with income distributed to him as aforesaid.

- ‘A’ wishes to start the business of ready-made garments but lacks the required funds for that business. ‘B’ agrees to participate with him for a specified period, say two years. 40% of the investment is contributed by ‘A’ and 60% by ‘B’. Both start the business on the basis of Diminishing Musharakah. The proportion of profit allocated for each one of them is expressly agreed upon. But at the same time ‘B’s share in the business is divided to six equal units and ‘A’ keeps purchasing these units on gradual basis until after the end of two years ‘B’ comes out of the business, leaving its exclusive ownership to A. Apart from periodical profits earned by ‘B’, he gains the price of the units of his share which, in practical terms, tend to repay to him the original amount invested by him.

Types of Diminishing Musharakah:

Shirkat-ul-Aaqd (Joint Venture):

FEATURES:

Two partners start business in Shirkah to earn profit. One of the partners undertakes to purchase the share of another partner gradually, each month or each year.

RULES:

- There will be an agreement of Shirkat-ul-Aqd between both partners where in investment of everyone and ratio of profit will be agreed.

- One partner undertakes to purchase the share of other partner. In this promise three conditions should be considered:

This promise will not be a part of Shirkah agreement. The price of unit will not be agreed in this promise but promise to purchase should be at market value at the time of purchasing.

- At the time of purchase, the price of unit will be decided on the basis of market value of business.

- Unit will be purchased through Offer & Acceptance.

Shirkat-ul-Milk (Joint Ownership):

Two partners purchase any asset (machinery/property) and their intention is that one or both partners will use this asset or they rent out their share and one share holder undertakes to purchase the share of other gradually.

RULES:

- There will be an agreement of Shirkat ul Milk and it will be decided How much investment will be made by each partner?

- Asset will be purchased and everyone will be owner of this asset as per ratio of his investment and all other rules of Shirkat-ul-Milk will be applicable

- One Shareek can rent out his share to other partner or to a third party and Ijarah Agreement will be signed.

- Within period of Ijarah, Shriah Ahkaam relating to Ijarah will be applicable.

- One of the partners can promise to purchase the share of another partner and in this promise; the price of unit may be decided.

- Unit can be purchased on the basis of Offer & Acceptance.

- All the above-mentioned agreements and undertaking should be independent and not tide-up with each other.

Diminishing Musharakah for Islamic Mortgage:

Diminishing Musharaka usually being used in House Financing for four purposes:

- Purchase of House.

- Construction of House.

- Renovation of House.

- Balance Transfer Facility (BTF).

FOR PURCHASE OF HOUSE:

- Client in the approved area of the bank makes the choice of house.

- Bank & client enter into Diminishing Musharakah agreement. In this agreement it is decided to purchase the house jointly and ratio of investment by each one.

- The both partners will be owner of that property in same ratio as ratio of investment.

- The property will be in the name of the client.

- This is Shirkat-ul-Milk.

- According to the ratio of ownership, each one is responsible for the loss.

- Bank divides its own part of asset into units, which is promised by the client to purchase on pre-agreed price.

- After taking possession of house, bank rent out its share to the client by execution of Ijarah Agreement.

- Rent may be fixed on prevailing market rate or with mutual consent.

- Bank’s monthly profit may also be decided, as monthly rent of the house and principal amount will be recovered in the unit price.

- In Ijarah Agreement, a lump sum amount of rent is necessary to be fixed for a certain period. Rent for the rest of the period, may be linked with agreed Benchmark.

- Each unit will be purchased on the basis of Offer & Acceptance.

FOR CONSTRUCTION OF HOUSE:

There are two scenarios:

- Financing for Purchase of Plot & Construction.

- Financing for Construction Only.

FINANCING FOR PURCHASING OF PLOT AND CONSTRUCTION:

- Diminishing Musharakah Agreement will be signed between bank and client in which investment of everyone will be agreed. It will also be agreed that client as working partner will be responsible for construction.

- The both partners will be owner of the property in same ratio as ratio of investment.

- The property will be in the name of the client.

- This is Shirkat-ul-Milk.

- According to the ratio of ownership, each one is responsible for the loss.

- Bank will divide its own part of asset into units, which is promised by the client to purchase on pre-agreed price.

- After completion of house, Ijarah Agreement will be signed and bank will give his share of house on rent to the client. Before completion of construction, rent cannot be charged.

- Rent may be fixed on prevailing market value or with mutual consent.

- Bank’s monthly profit may also be decided, as monthly rent of the house and principal amount will be recovered in the unit price.

- In Ijarah Agreement, a lump sum amount of rent is necessary to be fixed for a certain period. Rent for the rest of the period, may be linked with agreed Benchmark.

- Each unit will be purchased on the basis of Offer & Acceptance.

- Purchase of unit can be started after Diminishing Musharakah Agreement.

FINANCING FOR CONSTRUCTION OF HOUSE ONLY:

- Valuation of plot will be made. This value will be investment of client in Musharakah Agreement and bank’s financing for construction will be investment of bank.

- Musharakah Agreement will be signed between bank and client in which investment of everyone will be agreed. It will also be agreed that client as working partner will be responsible for construction.

- The both partners will be owner of the property in same ratio as ratio of investment.

- The property will be in the name of the client.

- This is Shirkat-ul-Milk.

- According to the ratio of ownership, each one is responsible for the loss.

- Bank will divide its own part of asset into units, which is promised by the client to purchase on pre-agreed price.

- After completion of house, Ijarah Agreement will be signed and bank will give his share of house on rent. Before completion of construction, rent cannot be charged.

- Rent may be fixed on prevailing market value or with mutual consent.

- Bank’s monthly profit may also be decided, as monthly rent of the house and principal amount will be recovered in the unit price.

- In Ijarah Agreement, a lump sum amount of rent is necessary to be fixed for a certain period. Rent for the rest of the period, may be linked with agreed Benchmark.

- Before one year, client cannot purchase bank’s units

- Each unit will be purchased on the basis of Offer & Acceptance.

FOR RENOVATION OF HOUSE:

- Valuation of house will be made and this value will be treated as investment of client in Diminishing Musharakah Agreement and renovation amount will be considered as bank’s investment.

- Diminishing Musharakah Agreement will be signed between bank and client in which investment of everyone will be agreed. It will also be agreed that client as working will be responsible for renovation.

- The both partners will be owner of the house in same ratio as ratio of investment.

- The property will be in the name of the client.

- This is Shirkat-ul-Milk.

- According to the ratio of ownership, each one is responsible for the loss.

- Bank will divide its own part of asset into units, which is promised by the client to purchase on pre-agreed price.

- After completion of renovation, Ijarah Agreement will be signed and bank will give his share of house on rent. Before completion of renovation, rent cannot be charged.

- Rent may be fixed on prevailing market value or with mutual consent.

- Bank’s monthly profit may also be decided, as monthly rent of the house and principal amount will be recovered in the unit price.

- In Ijarah Agreement, a lump sum amount of rent is necessary to be fixed for a certain period. Rent for the rest of the period, may be linked with agreed Benchmark.

- Before one year, client cannot purchase bank’s units.

- Each unit will be purchased on the basis of Offer & Acceptance.

FOR BTF:

- This product will be used only in those cases where someone have obtained interest-based loan for house.

- Valuation of house will be made and this value will be treated as investment of client in Diminishing Musharakah Agreement and amount of loan paid by bank will be investment of bank.

- The agreement will be signed between bank and client in which investment of everyone will be agreed.

- Both partners will be owner of the property in same ratio as ratio of investment.

- The property will be in the name of the client. This is Shirkat-ul-Milk.

- According to the ratio of ownership, each one is responsible for the loss.

- Bank will divide its own part of asset into units, which is promised by the client to purchase on pre-agreed price.

- Ijarah Agreement will be signed and bank will give his share of house on rent to the client.

- Rent may be fixed on prevailing market value or with mutual consent.

- Bank’s monthly profit may also be decided, as monthly rent of the house and principal amount will be recovered in the unit price.

- In Ijarah Agreement, a lump sum amount of rent is necessary to be fixed for a certain period. Rent for the rest of the period, may be linked with agreed Benchmark.

- Before one year, client cannot purchase bank units.

- Each unit will be purchase on the basis of Offer & Acceptance.

This lecture is designed for Islamic banking and finance courses, diploma Islamic banking, and masters in Islamic banking and finance programs, which are offered by AIMS. Here is another lecture on accounting in Islamic banking.