What is Project Cost Management?

Let us first understand what is project cost management? Cost management in project management allows a business to predict impending expenditures to help reduce the chance of going over budget. Project Cost Management includes each and every cost of the project (to execute every process), from planning to execution, so the project can be completed in a given budget.

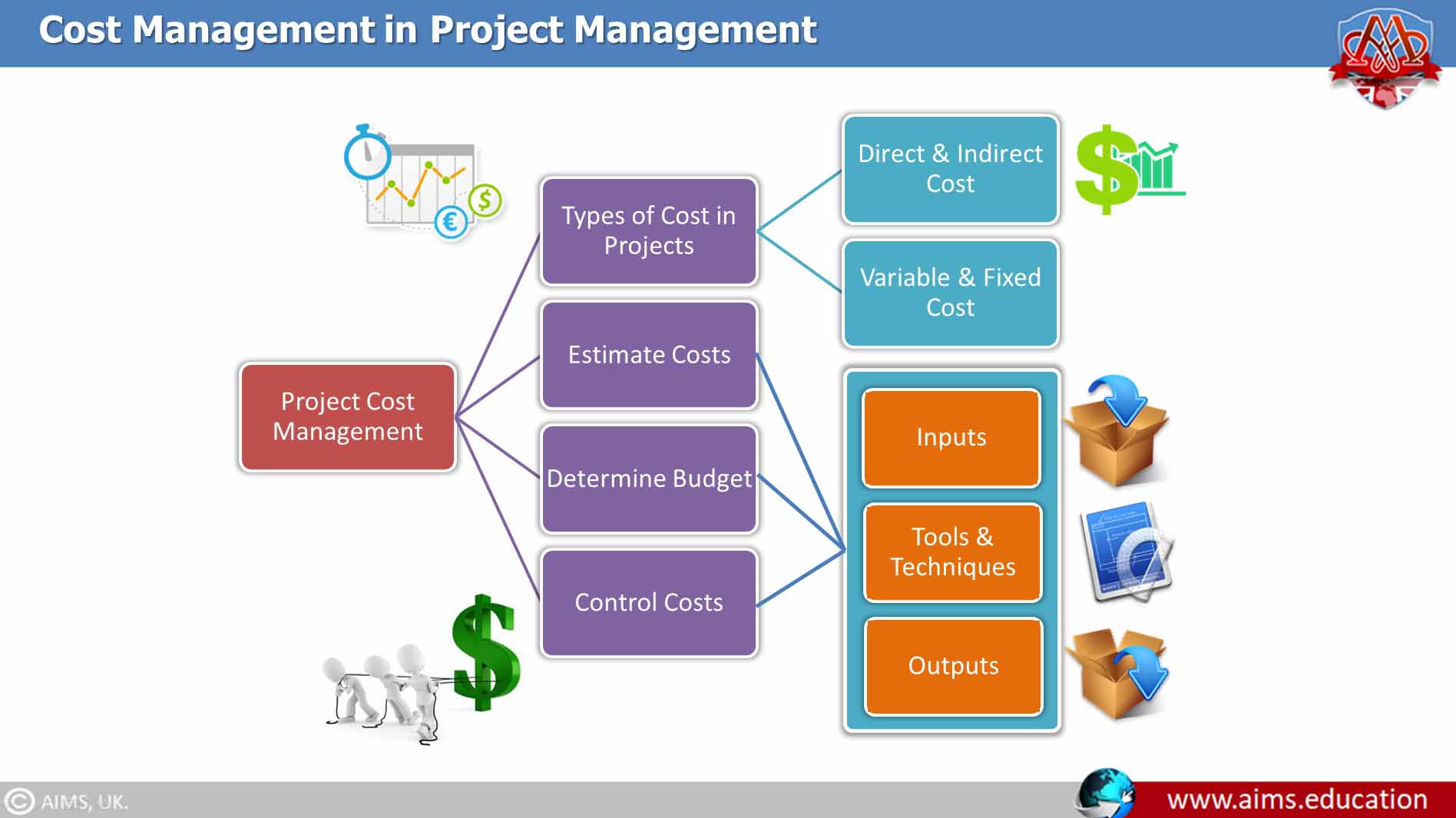

Cost Management in Project Management:

Two of the most important documents you’ll prepare for any project are the project schedule and the project budget. You’ll use the schedule and budget documents throughout the Executing and Monitoring and Controlling processes to measure progress and determine if the project is on track.

Unlike project quality management, there are two processes in the Planning group we’ll perform that will lead us to the cost performance baseline output that is the authorized budget. They are Estimate Costs and Determine Budget. There are several tools and techniques to cover in these processes. There is one process in Monitoring & controlling group, Control Costs that is used to manage the changes in the cost baseline.

A brief overview of processes for cost management in project management are as follows:

- Estimate Costs—The process of developing an approximation of the monetary resources needed to complete project activities.

- Determine Budget—The process of aggregating the estimated costs of individual activities or work packages to establish an authorized cost baseline.

- Control Costs—The process of monitoring the status of the project to update the project costs and managing changes to the cost baseline.

Estimate Project Cost:

The Estimate Costs process in project cost management develops a cost estimate for the resources (human and material) required for each schedule activity. This includes weighing alternative options and examining risks and trade-offs. Some alternatives you may consider are make-versus-buy, buy-versus-lease, and sharing resources across either projects or departments.

Let’s look at an example of trade-offs. Many times software development projects take on a life of their own. The requested project completion dates are unrealistic; however, the project team commits to completing the project on time and on budget anyway. How do they do this? They do this by cutting things such as design, analysis, and documentation. In the end, the project might get completed on time and on budget, but was it really? The costs associated with the extended support period because of a lack of design and documentation and the hours needed by the software programmers to fix the reported bugs weren’t included in the original cost of the project (but they should have been). Therefore, the costs actually exceed what was budgeted. You should examine trade-offs such as these when determining cost estimates. The project management office sometimes plays an important role for the estimation of cost management in project management.

Estimate Costs Inputs:

Many of the inputs of the Estimate Costs process are already familiar to you. However, we’ll look briefly at each one so you can see the key elements that should be considered when creating the project budget. Cost management in project management explains the inputs to this process, are as follows:

- Project baseline.

- Project schedule.

- Human resource plan.

- Risk register.

- Enterprise environmental factors.

- Organizational process assets.

Tools and Techniques to Estimate Costs:

Estimate Costs has nine tools and techniques used to derive estimates:

- Expert judgement.

- Analogous estimating.

- Parametric estimating.

- Bottom-up estimating.

- Three-point estimate.

- Reserve analysis.

- Cost of quality.

- Project management estimating software.

- Vendor bid analysis.

Estimate Costs Process: Outputs:

Activity Cost Estimates:

Activity cost estimates in project cost management are quantitative assessments of the probable costs required to complete project work. Cost estimates can be presented in summary form or in detail. Costs are estimated for all resources that are applied to the activity cost estimate. This includes, but is not limited to, direct labor, materials, equipment, services, facilities, information technology, and special categories such as cost of financing (including interest charges), an inflation allowance, exchange rates, or a cost contingency reserve.

Basis of Estimates: Basis of estimates is the supporting detail for the activity cost estimates and includes any information that describes how the estimates were developed, what assumptions were made during the Estimate Costs process, and any other details you think are needed. According to the PMBOK® Guide and as you can find details in project management degree, postgraduate diploma in project management, and masters in project management. The basis of estimates should include at least the following:

- A description of how the estimate was developed or the basis for the estimate.

- A description of the assumptions made about the estimates or the method used to determine them.

- A description of the constraints

- A range of possible results. You should state the cost estimates within ranges such as $5000 ± 10%.

- The confidence level regarding the final estimates.

Estimate Project Budget Baseline:

The next process in the project cost management concerns determining the cost performance baseline, which is the primary output of the Determine Budget process. The Determine Budget process aggregates the cost estimates of activities and establishes a cost performance baseline for the project that is used to measure performance of the project throughout the remaining process groups. An important goal of cost baseline is to provide info for project funding requirements –at what point(s) in time will the money be needed Only the costs associated with the project become part of the authorized project budget. For example, future period operating costs are not project costs and therefore aren’t included in the project budget.

Determine Budget Inputs:

In order to understand what is project cost management, let us first explain the budget inputs. Outputs from other Planning processes, including the Create WBS, Schedule Development, and Estimate Costs processes, must be completed prior to working on Determine Budget because some of their outputs become the inputs to this process. The inputs for Determine Budget are as follows:

ACTIVITY COST ESTIMATES:

These are an output of the Estimate Costs process. Activity cost estimates are determined for each activity within a work package and then summed to determine the total estimate for a work package.

BASIS OF ESTIMATES:

This is also an output of the Estimate Costs process and contains all the supporting detail regarding the estimates. You should consider assumptions regarding indirect costs and whether they will be included in the project budget. Indirect costs cannot be directly linked to any one project. They are allocated among several projects, usually within the department or division in which the project is being performed. Indirect costs can include items like building leases, management and administrative salaries (those not directly assigned full time to a specific project), and so on.

SCOPE BASELINE:

Scope baseline includes the scope statement, WBS, and WBS dictionary. The scope statement describes the constraints of the project you should consider when developing the budget. The WBS shows how the project deliverables are related to their components, and the work package level typically contains control account information (although control accounts can be assigned at any level of the WBS).

PROJECT SCHEDULE:

Project cost management schedule contains information that is helpful in developing the budget, such as start and end dates for activities, milestones, and so on. Based on the information in the schedule, you can determine budget expenditures for calendar periods.

RESOURCE CALENDERS:

Resource calendars help you determine costs in calendar periods and over the length of the project because they describe what resources are needed when on the project.

CONTRACTS:

Contracts include cost information you should include in the overall project budget. We’ll talk more about contracts in Procurement Management. Organizational process assets: The organization process assets that will assist you with the work of this process include cost budgeting tools, the policies and procedures your organization (or PMO) may have regarding budgeting exercises, and reporting methods.

Determine Budget Tools and Techniques:

The Determine Budget process has five tools and techniques, including two you haven’t seen before:

- Cost aggregation.

- Reserve analysis.

- Expert judgement.

- Historical relationships.

- Funding limit reconciliation.

Determine Budget: Outputs

In context for cost management in project management, the goal of Determine Budget is to develop a cost performance baseline for the project that you can use in the Executing and Monitoring and Controlling processes to measure performance. You now have all the information you need to create the cost performance baseline. In addition, you’ll establish the project funding requirements.

The following are the outputs of the Determine Budget process:

- Cost performance baseline

- Project funding requirements

- Project document updates

We have covered the project cost management document updates in other processes. For Determine Budget, you may need to update the risk register, cost estimates, and/or the project schedule.

Control Costs:

Control Costs is the process of monitoring the status of the project to update the project costs and managing changes to the cost baseline. The key benefit of this process is that it provides the means to recognize variance from the plan in order to take corrective action and minimize risk.

The key to effective cost control is the management of the approved cost baseline and the changes to that baseline. Project cost control includes:

- Influencing the factors that create changes to the authorized cost baseline.

- Ensuring that all change requests are acted on in a timely manner.

- Ensuring that cost expenditures do not exceed the authorized funding.

- Monitoring cost performance to isolate and understand variances from the approved cost baseline.

- Monitoring work performance against funds expended.

- Bringing expected cost overruns within acceptable limits.

Control Costs: Inputs:

COST BASELINE:

The cost baseline is compared with actual results to determine if a change, corrective action, or preventive action is necessary.

PROJECT FUNDING REQUIREMENTS:

The project funding requirements include projected expenditures plus anticipated liabilities.

WORK PERFORMANCE DATA:

Work performance data includes information about project progress, such as which activities have started, their progress, and which deliverables have finished. Information also includes costs that have been authorized and incurred.

ORGANIZATIONAL PROCESS ASSETS:

Existing formal and informal cost control-related policies, procedures, and guidelines; Cost control tools; and Monitoring and reporting methods to be used.

Control Costs: Tools and Techniques:

The tools and techniques of the Control Costs process are as follows:

- Earned value measurement (EVM)

- Forecasting

- To-complete performance index (TCPI)

- Performance reviews

- Variance analysis

- Project management software

We’ll look at each of these next with the exception of project cost management software. This output has been discussed previously, but you should know that in this process it can help automate and calculate the formulas we’re going to examine next. It can also display the results in graphical form for status reporting purposes.

Earned Value Management:

You can accomplish performance measurement analysis using a technique called earned value measurement (EVM). Simply stated, EVM compares what you’ve received or produced to what you’ve spent. The EVM continuously monitors the planned value, earned value, and actual costs expended to produce the work of the project. When variances that result in cost changes are discovered (including schedule variances and cost variances), those changes are managed using the project change control system. The primary function of this analysis technique is to determine and document the cause of the variance, to determine the impact of the variance, and to determine whether a corrective action should be implemented as a result.

FORECASTING:

Forecasting uses the information you’ve gathered to date and estimates the future conditions or performance of the project based on what you know when the calculation is performed. Forecasts are based on work performance information (an output from the Executing process group) and your predictions of future performance.

Control Costs: Outputs:

WORK PERFORMANCE INFORMATION:

The calculated CV, SV, CPI, SPI, TCPI, and VAC values for WBS components, in particular the work packages and control accounts, are documented and communicated to stakeholders.

COST FORECASTS:

Either a calculated EAC value or a bottom-up EAC value is documented and communicated to stakeholders.

CHANGE REQUESTS:

Analysis of project performance may result in a change request to the cost baseline or other components of the project cost management plan. Change requests may include preventive or corrective actions, and are processed for review and disposition through the Perform Integrated Change Control process.

PROJECT MANAGEMENT PLAN UPDATES:

Elements of the project management plan that may be updated include, but are not limited to; Changes to the cost baseline are incorporated in response to approved changes in scope, activity resources, or cost estimates. Changes to the cost management plan, such as changes to control thresholds or specified levels of accuracy.

PROJECT DOCUMENT UPDATES:

Project cost management documents that may be updated include, but are not limited to: Cost estimates, and Basis of estimates.